Understanding Loan Amortization and Its Importance

This article explains loan amortization, detailing how fixed payments reduce debt over time. It covers creating amortization schedules, types of loans that utilize amortization, and practical tips for managing debt effectively. A useful guide for borrowers to understand repayment progress and interest costs throughout their loan's duration.

Understanding Loan Amortization

Amortization refers to the process of gradually paying off a loan through fixed periodic payments over time. While the amount paid towards interest and principal can fluctuate monthly, the total payment remains consistent. Besides loans, amortization also describes allocating costs over an asset's lifespan, especially for intangible assets in accounting.

Each installment directly covers interest costs and reduces the outstanding principal balance. Initially, most payments go toward interest, with minimal impact on the principal, requiring patience and a clear understanding of your loan structure.

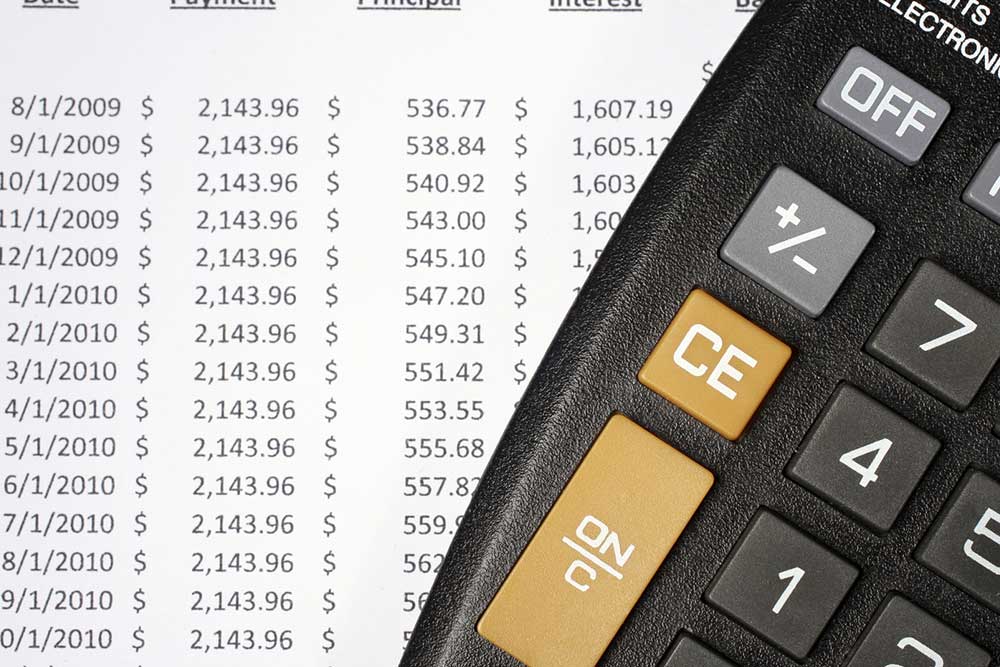

Creating an amortization schedule helps you visualize how your payments are allocated over the loan term. It can be done manually, via online calculators, or spreadsheet tools, providing clarity on repayment progress and interest costs.

Key steps in developing a schedule include:

Starting with your initial loan balance

Calculating your regular payment amount

Determining monthly interest charges

Deducting interest from the payment to find the principal repayment

Updating the remaining loan balance

Repeating this process for subsequent months

Various loan types utilize amortization, including:

Home Loans

Typically spanning 15-30 years with fixed interest rates. Borrowers can choose to refinance or sell the property before the loan's end, but consistent payments help clear the debt efficiently.

Personal Loans

Usually offered by banks or online lenders, these are short-term, fixed-rate loans for small projects or debt consolidation, often lasting around three years.

Auto Loans

Note:

Our blog provides practical insights across various topics. While our research aims to inform, readers should consider verifying information independently. We are not responsible for discrepancies or inaccuracies and acknowledge potential missed schemes or offers beneficial to readers.